Why tax should never drive investment decisions

Ta saving not the end goal Every few months, a story does the rounds that most of us read with envy and bewilderment. Somebody has

Ta saving not the end goal Every few months, a story does the rounds that most of us read with envy and bewilderment. Somebody has bought an apartment in one of those Gurugram towers that the developer insists on naming after flowers—the Arallias, the Camellias, the Magnolias, and now the Dahlias—for a sum with enough zeros to buy a village.The most recent had one of the country’s best-known stock market investors, a name most of you would recognise, paying around Rs.120 crore for a single flat. The reaction of the ordinary mortal is to assume there must be a clever tax reason behind it, based on the belief that nobody that rich does anything without first consulting a tax adviser.Maybe there is one, but my own belief is it has little to do with tax and a great deal to do with the oldest motive: the wish to own something that announces that one has arrived.Think of what the tax law has on offer here.

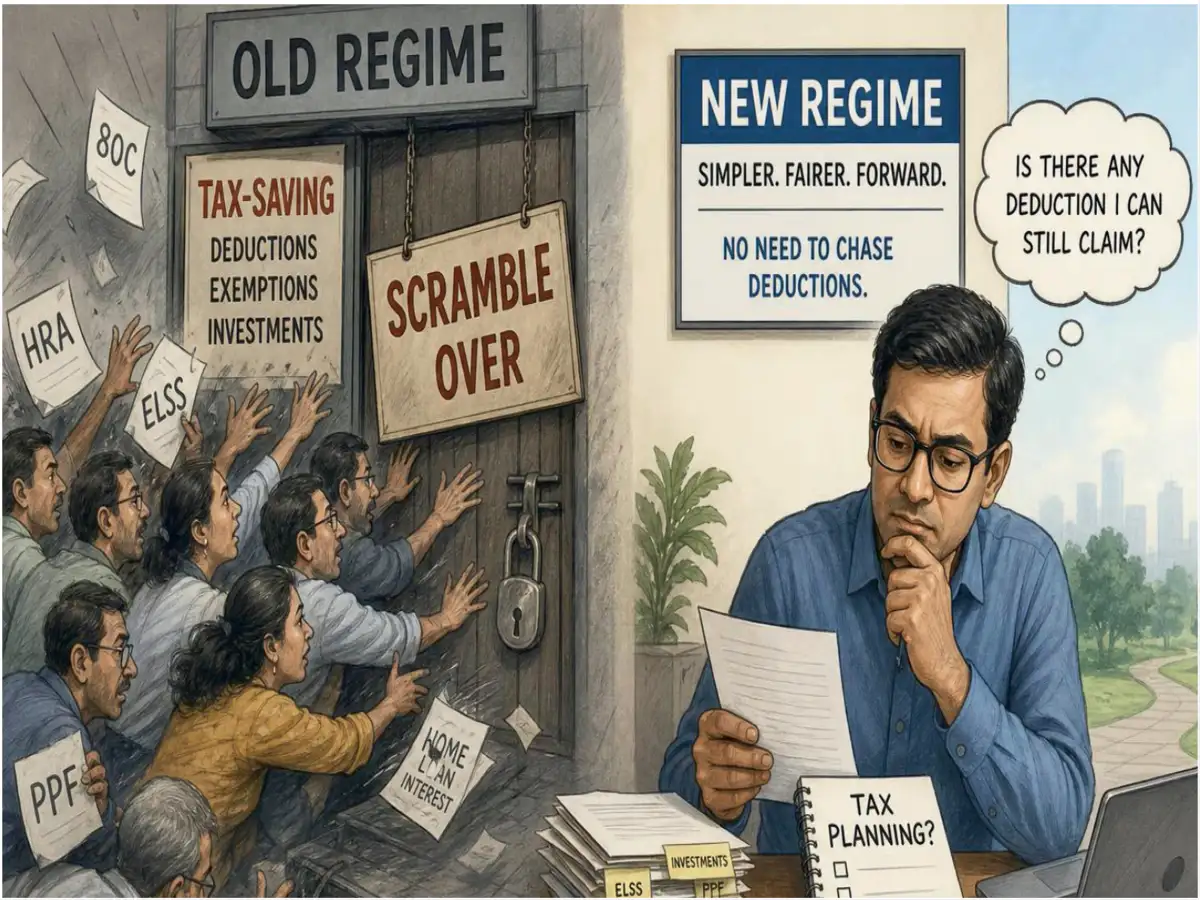

If you sell shares and pour the proceeds into a house, part of your capital gain can escape tax, but the maximum that is exempt is Rs.10 crore which, against a flat of Rs.120 crore, is just a rounding error. The taxman has not been outwitted—the man has just bought a very expensive home, as the wealthy always do.I’m discussing this because for most of my writing life, the tax mistake that hurt ordinary savers was the opposite. Every February, the same ritual used to play out: a saver who had ignored the matter all year would recall the deadline and, in the last fortnight of March, buy an endowment policy heavy with commission or a five-year deposit paying a whisker above inflation, then console himself that at least he had saved some tax. The point I kept making was that an investment must first stand up as an investment, and be a ta saver only by accident.However, this problem has now solved itself.

The new tax regime, now the default and chosen by close to three in four taxpayers, has done away with such deductions. Where there is no Section 80C to chase, there is no reason to go shopping for the bad product in March. The government did not reform anyone’s behaviour—it just removed the bait, and that worked just as well.But the instinct behind all that has not died with the deduction. The willingness to let the tax tail wag the investment dog has merely climbed the wealth ladder to the one tax that still bites—capital gains, whose various shelters survived the new regime untouched. However, they do their real harm not to the Camellia-Dahlia types, but those with a couple of fewer zeros.There is the man who has done well in equities, holding something liquid and diversified, who is talked into turning the lot into a single illiquid flat because the tax saved feels like money found lying on the road. And there is the one who locks fifty lakh into a government bond paying 5% for five years, every rupee of it taxable, to escape a 12.5% tax he could have paid once and forgotten.