Astral's demerger plan triggers sharp market selloff, brokerages trim targets

ET Intelligence Group: Shares of Astral, a manufacturer of plumbing products and construction chemicals, have fallen 11% since Monday after the company announced plans to

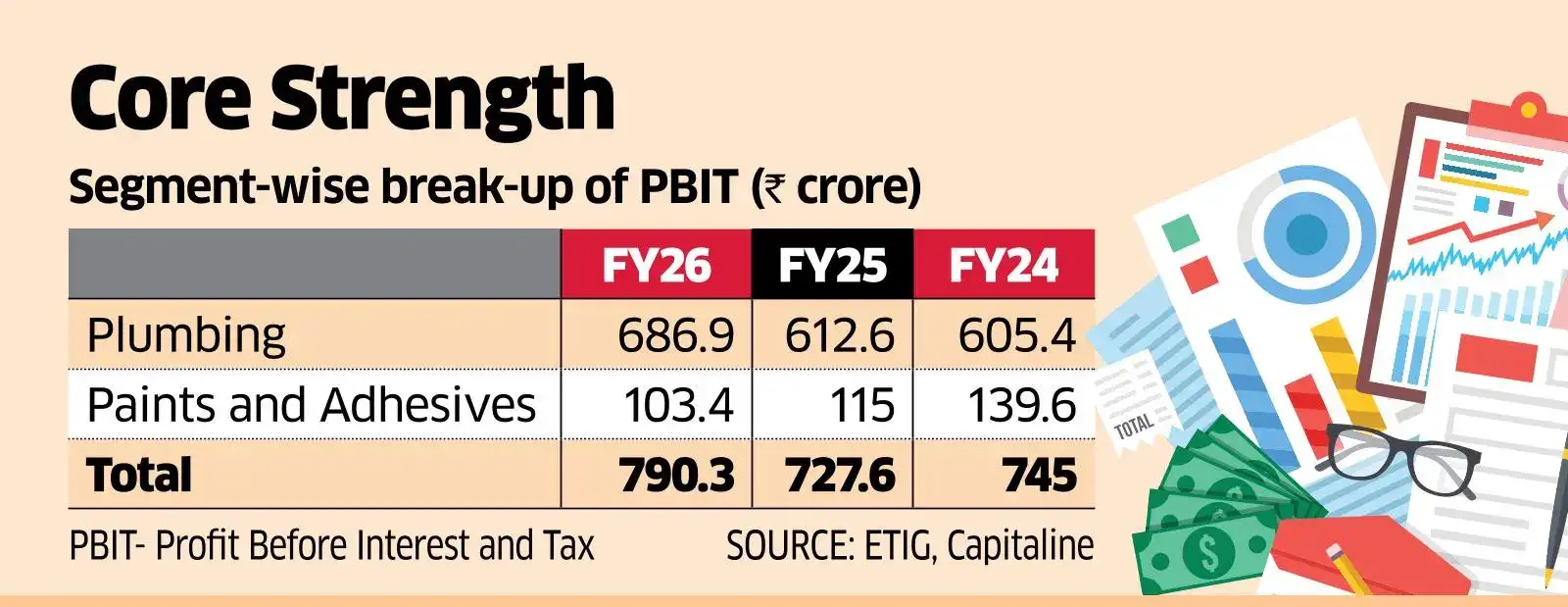

ET Intelligence Group: Shares of Astral, a manufacturer of plumbing products and construction chemicals, have fallen 11% since Monday after the company announced plans to demerge its chemicals business from the core plumbing operations. The fall can be attributed to uncertainty over the standalone valuation and growth prospects of the demerged entity. At present, the chemicals business generates lower margin and slower revenue growth compared with the plumbing segment. Analysts have reduced target prices by 5-9%.On June 25, Astral announced plans to demerge the adhesives, paints and construction chemicals business into a separately listed company, while retaining its plumbing business in the existing listed entity."Adhesive plus paint business valuations will be the tricky part as how much discount it gets versus listed peers is difficult to comprehend," said Equirus Securities in a report, adding that the smaller scale of this business makes it difficult to estimate the multiple it will command after the demerger.132150433The plumbing business has increasingly become Astral's earnings and cash-flow engine with its Profit Before Interest and Tax (PBIT) rising to ₹686.9 crore in FY26 from ₹605.4 crore in FY24.

On the contrary, PBIT of the chemicals business declined to ₹103.4 crore from ₹139.6 crore. As a result, the plumbing division's contribution to the total PBIT increased to nearly 87% from about 81% during the period.In FY26, the plumbing business contributed around 71% of the total ₹6,569 crore revenue. Brokerages have retained their 'buy' ratings on Astral, although some have cut their target prices by 5-9% following the demerger announcement.Management expects revenue from the chemical business to grow to ₹4,400-5,000 crore over the next four to five years from ₹1,861 crore in FY26, implying an annual growth rate of 19-22%.

The company will disclose separate Profit and Loss statements and balance sheets for both entities along with the June quarter of FY27 results."We expect the creation of a separate entity to lead to some cost increases, along with

potential operational disruptions during the demerger process," stated HDFC Securities in a report. The broker maintained a 'buy' rating on the stock with a target price of ₹1,740. The stock closed Thursday's session at ₹1,364.6 on the BSE.